Fraud susceptibility increases during times of chaos, and that, coupled with today’s supply chain weakness, intensifies the pressure companies are facing to mitigate international trade risk.

International Transactions Risks and Challenges

Representing International Risks and Challenges, “Counterparty” points to “Country” which points to “Bank” which points back to “Counterparty”.

Banks play a central role in the provision of trade finance and credit, acting as financial and processing intermediaries that plug the gap between sellers’/exporters’ demands of optimizing (i.e. shortening) Days Sales Outstanding (DSO) and buyers’/importers’ preference for extending Days Payables Outstanding (DPO).

Business opportunities abound on the global level, but international transactions tend to be trickier to structure and manage, in addition to being riskier. Without having easy access to reliable information on foreign counterparties, or even local knowledge, it can be difficult to ascertain the likelihood that proposed transactions are real and will be paid as agreed.

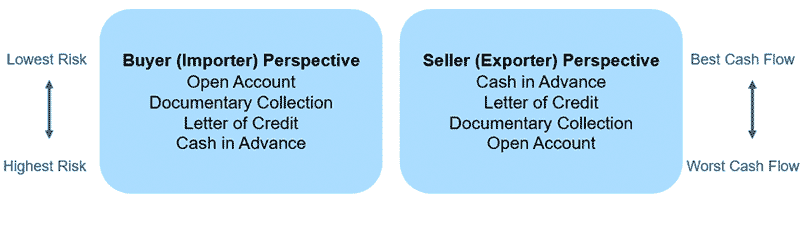

Generally speaking, there are several payment methods available in a transaction, and buyer and seller have reversed priorities as to suitability:

Buyer / Seller

For the Buyer (Importer), from lowest risk to highest risk, payment methods include Open Account, Document Collection, Letter of Credit, and Cash in Advance.

For the Seller (Exporter), from best cash flow to worst cash flow, payment methods include Cash in Advance, Letter of Credit, Documentary Collection, and Open Account.

Because buyers and sellers should have contrary priorities, it is important to confirm that your company is protected to the greatest degree possible from transactional risk.

Letters of credit (LCs) are a great way to help mitigate risk, and if structured properly, can help offer peace of mind. The level of protection depends upon the wording / structuring of the LC, as well the issuing / confirming bank and country. Outlined below are important considerations when transacting under LC terms, as well as available alternative risk-mitigation products.

Top Ten Considerations for LCs and Other International Trade Solutions

1. Evaluate the Effect on Credit Utilization

A common strategy by companies in the early stages of the Covid-19 pandemic was to draw down on credit lines to shore up cash balances. During a 3-week period in March 2020, more than 130 companies in Europe and the Americas drew at least $124 billion.[1] Increased credit utilization could adversely affect a company’s ability to issue LCs, as any issuance will tie up their credit line for the amount of each issuance. These credit implications apply to both import letters of credit issued to pay for foreign goods and to standby letters of credit issued to back up ongoing purchases and for performance related assurances for some US exporters of goods and services.

For companies looking to mitigate risk with international trade, properly structured LCs can address concerns of payment in full and on time, and hold sellers to the terms of their purchase orders, even with historically proven trading associates.

Keep in mind that an LC issued by your buyer’s bank and in your favor has no effect at all on your domestic credit facility.

2. Review LC Wording and Accuracy

LCs can only be drawn by the beneficiary if the terms and conditions in the LC are met, so it is extremely important that exporters are comfortable with the wording of the LC. As a best practice, LC drafts should be produced and closely reviewed by both parties, before any LC is formally issued. Amending an LC after it is issued takes time and money. Considerations should be given to accuracy of information, latest shipment date and expiry date, minimum documentation requirements, and where possible, eliminating any need for documents to be produced by 3rd parties.

3. Consider a Confirmation

If you have concerns about the country or the LC issuing bank itself, or if your company’s policy is to limit or eliminate foreign risk, consider a confirmation. Ideally, a confirmation would be provided by your own bank, but in any case by a bank in your home country. It effectively transfers risk of payment from that of the issuing bank and its country to that of the confirming bank and its country.

Confirmation gives rise to another bank charge, calculated on how risky the issuing bank is considered by the confirming bank. Ideally this charge can be quoted up front, to allow for its inclusion in the pricing of the underlying product and/or sales contract.

4. Calculate the Benefits of Discounting

LC payment terms can be made to align with the terms of your sales contract. As an example, if payment terms under the sales contract are 90 days from shipment, the LC can reflect those same terms and pay out 90 days after the bill of lading date. In such LCs, the beneficiary should consider discounting that payment, which does not touch his domestic credit facility, and can at times be accomplished at a cheaper all-in rate than accessing his domestic line.

5. Leverage Standby LCs for Ongoing Relationships

If you are buying on an ongoing basis from the same supplier, a standby LC might be less expensive for both parties, depending on the frequency of sales. This standby arrangement would allow the seller to operate on open account terms, as long as the amount outstanding and owed at any time does not exceed the nominal value of the standby.

Equally important is the expiration date, which should be regularly monitored to confirm no gap in coverage. An auto-extension provision can ease the burden of monitoring, as it allows the standby to automatically extend annually unless a formal written notice is delivered to the beneficiary. It is important to underscore that standbys, as usually worded, favor the beneficiary over the applicant, so caution in the wording and in to whom it is offered is very important.

6. Local Bank Guarantees

When the overseas beneficiary demands payment security in the form of a local bank guarantee, your domestic bank can issue a standby LC in favor of a local bank in the country of the beneficiary. That standby will serve as a counter guarantee for the local bank to issue its own instrument – usually governed by local law and often in the local language.

This structure is not optimal as it is costly, negotiation of wording is difficult and time-consuming, and guidance lines must exist between both banks which is not always the case. Where possible, companies should negotiate out of local bank guarantee requirements, and allow their bank to issue standby letters of credit directly to the beneficiary, advised through their bank.

7. Documentary Collection Risk

Documentary collections provides less risk mitigation than a letter of credit, but they have the advantage of being widely used for ongoing sales where contract repudiation is not a concern of the seller – either because the product can easily be resold or redirected to another buyer or where an ongoing and/or distributor type arrangement is in place. Documentary collections are much less expensive than either a letter of credit or credit insurance (see below), and are not a user of credit for either buyer or seller. There is one main risk with documentary collections, and that is the buyer’s ability to refuse the documents upon arrival, thereby exposing exporters to contract frustration / repudiation risk.

8. Credit Insurance

Credit insurance is an alternative to LCs for risk mitigation. More widely used in Western Europe than in North America, sellers obtain commercial and political risk coverage on their short term export receivables under programs / policies offered by both the US government’s Export-Import Bank of the United States (see #9 below) and by a number of reputable private sector providers. An independent credit insurance broker can provide unbiased advice on the best insurer for an exporter’s particular needs.

There are pros and cons to credit insurance versus LCs. Credit insurance does not offer the 100% payment coverage of an LC, and it has deductibles, insurance premium payment, reporting requirements and coverage exclusions for things like product disputes. Importantly, its cost is normally borne by the seller / exporter, so the buyer / importer does not need to access his bank credit facility.

Also, an exporter may find that his insured export receivables can be accepted by his domestic bank as part of a borrowing base, whereas uninsured foreign receivables would normally be entirely excluded from such considerations.

9. The Export-Import Bank of the United States - EXIMBANK

EXIMBANK, despite having the word “Import” in its title, is entirely focused on US exporters by providing financing to eligible international buyers and pre-export financing. EXIMBANK is a full faith and credit US government agency lending support to exporters through a number of programs. Two of its programs are aimed at reducing or eliminating the foreign account receivables of US exporters – short term credit insurance and longer term guarantees -- and the other is to get pre-export funding into the exporters’ hands – the working capital guarantee program. Two of these three programs are accessed through your commercial banking associate and the other through a credit insurance broker or via EXIMBANK directly.

While EXIMBANK has not relaxed their credit criteria, they have recently introduced a number of temporary measures to make things easier for users of their existing export-promotion programs, like extending deadlines for reporting, premium payments, claim filing and interest payments, allowed additional collateral.

10. Force Majeure

In general terms, force majeure is understood to mean the interruption of its business by acts of God, riots, civil commotions, insurrections, wars, acts of terrorism, or by any strikes or lockouts or any other causes beyond its control.

As the concept of force majeure applies to letters of credit, strong trade banks should continue to honor obligations under letter of credit they have issued or confirmed, if documents are presented to them while the letter of credit is still valid and the banks are open for business. But that does not mean that the concept will not affect how the banks handle letters of credit. The slowness or shutdown of courier services in some countries affects the flow of letters of credit, yet late arrival of documents at a bank is not in itself a force majeure event, although it could be a consequence of one.

Historically, letters of credit have required physical delivery of documents, and customs authorities typically permit clearing and taking possession of goods against an original, signed title document. However, due to the Covid-19 pandemic and supported by eUCP, some trade banks are accepting scanned documents via e-mail, with SWIFT or telephone verification.

The International Chamber of Commerce regulations governing letters of credit deal with force majeure in different ways. ISP98 and UCP600 can apply to standby letters of credit, whereas UCP600 applies only to documentary L/Cs.

Article 36 of UCP600 states not only that a bank assumes no liability or responsibility for the consequences arising out a force majeure event, but importantly that a bank will not, upon resumption of its business, honor or negotiate under a credit that expired during such interruption of its business. It is possible, and desirable for a beneficiary, to ask for wording in the LC allowing presentation after resumption of business, notwithstanding this Article 36.

ISP98 Rule 3.14 states that if on the last business day for presentation the place for presentation stated in a standby is for any reason closed and presentation is not timely made because of the closure, then the last day for presentation is automatically extended to the day occurring thirty calendar days after the place for presentation re-opens for business, unless the standby otherwise provides.

COVID-19 Observed Trends

Global lockdowns are creating challenges and opportunities in financing and servicing trade transactions:

- Some slowdown and obstacles with payments and trade transactions from/to emerging markets (e.g. India)

- Disruptions with clients’ supply chain (China, some European markets)

- Global difficulties in paper-based documentary deliveries by international couriers, varying interpretations of force majeure in different legal jurisdictions

- Accelerated evaluation and use of SWIFT FileAct and other electronic solutions to deliver digitized trade LC documents

- Increasing requests for letter of credit confirmations

- Requests for cash in advance to pay for protective personal equipment (PPE), many are fraudulent

- Increased demand for payments and information automation, as well as outsourcing alternatives (i.e. Canadian lockbox)

Ready to Help

Mitigating risk has never been more important, and there are many considerations that companies need to manage when transacting globally. The considerations outlined in this whitepaper are just some, so please contact your International Advisor at PNC as we are happy to collaborate with your clients to help protect your business.