Revisión del mercado: May flowers

Global equities extended their rally in May as investors remained focused on economic strength and the artificial intelligence (AI) cycle. The S&P 500® closed the month at another record high. Strong earnings results and forward guidance — combined with sustained AI demand for semiconductor chips — led to outperformance by the MSCI Emerging Market and Nasdaq indices, given their heavier exposure to the Information Technology sector.

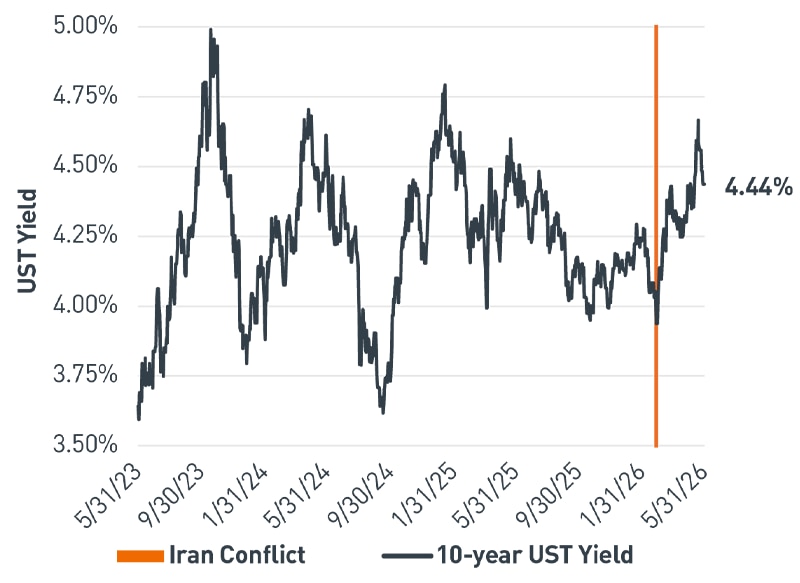

Conflicting headlines surrounding the progress of U.S.-Iran conflict negotiations caused whiplash in global energy and bond markets in May. Crude oil prices increased throughout most of the month, before finishing modestly lower. Inflation passthrough risks continued to weigh on the bond market, with the 10-year U.S. Treasury (UST) yield reaching 4.67% mid-month — its highest level since the Iran conflict began in February — before moderating (Figure 1).

Figure 1. 10-year U.S. Treasury yield

In mid-May, Treasury yields hit their highest level since the Iran conflict began in February

A partir del 05/31/2026. Fuente: Bloomberg L.P.

Ver la versión accesible de este gráfico.

Notas breves

Interest rates are back in focus

- The equity market may have greater sensitivity to further rises in the 10-year UST yield if it pushes higher from current levels.

- The increase in long-term rates is partly inflation-driven and partly from a rise in real yields.

Continued dispersion across sectors

- A handful of sectors — including Consumer Staples, Consumer Discretionary and Industrials — had negative second-quarter earnings revisions.

Consumer sentiment hits an all-time low

- The University of Michigan Consumer Sentiment Index declined to an all-time low.

- These strains suggest uneven outcomes across industries and consumers.

The big picture: AI momentum remains strong…for now

To close out May, the S&P 500 increased for a ninth consecutive week, driven by AI-related technology stocks, which in turn have been driven by significant capital spending. For 2026, the mega-capitalization (cap) “Magnificent 7” tech companies have announced capital expenditure (capex) plans exceeding $700 billion — more than 2% of U.S. GDP and approximately 60% higher than 2025 levels. This capex also has a significant multiplier effect, as one company’s expenditure is another company’s revenue, which then allows for further spending down each layer of the supply chain.

At this time last year, much of the AI narrative was dominated by concerns of “circular financing,” whereby certain suppliers or service providers took equity stakes in AI model developers in exchange for cash that was then used, in part, to purchase more supplies. Since then, rapid AI adoption and the rollout of productivity-enhancing packages have tempered — if not reversed — much of that skepticism. Throughout this time, our position has been consistent: we believe the economic benefits of AI will be substantial and create a once-in-a-generation productivity boom.

Among leading AI companies, the race to build advanced models remains intense. Much of the outsized capex thus far has been made by companies that consider leadership in AI to be an existential need. While this may hold true for a subset of AI-focused companies, we expect most companies to adopt AI as a tool to support their core businesses. As such, we believe there is increased risk of a slowdown in capex growth once the initial phase of accelerated investment transitions into a more sustainable, longer-term pace. In the near term, however, we expect mega-cap tech companies to continue to invest aggressively with capex, rather than pull back.

Perspectiva y posicionamiento de la cartera

El consenso del mercado se está consolidando en torno a nuestra postura de larga data de que la economía se encuentra en medio de un sólido ciclo de inversión empresarial y productividad impulsado por la IA. While higher gasoline and diesel prices may lead to cost pressure and plateau consumer spending, the boom led by AI infrastructure capex does not yet appear to be exhausted. We believe this trend will continue to underpin equity markets in the near term, and combined with strong earnings, supports our tactical tilt towards equities with an emphasis on AI-related technology companies in the U.S. and emerging markets.

VERSIÓN TEXTUAL DE LOS GRÁFICOS

Figure 1. 10-year U.S. Treasury yield (view image)

In mid-May, Treasury yields hit their highest level since the Iran conflict began in February

Fecha |

Rendimiento de bonos del Tesoro de EE. UU. a 10 años |

05/31/23 |

3.64 % |

09/30/23 |

4.57 % |

01/31/24 |

3.91 % |

05/31/24 |

4.50 % |

09/30/24 |

3.78 % |

01/31/25 |

4.54 % |

05/31/25 |

4.40 % |

09/30/25 |

4.15 % |

01/31/26 |

4.24 % |

05/31/26 |

4.44 % |

A partir del 05/31/2026. Fuente: Bloomberg L.P.