Since 2023, PNC Healthcare has engaged hospitals and health systems in its annual Provider Survey to better understand where they are focused, the industry trends they are excited about, and the headwinds of greatest concern. The respondents in 2023 – the aftermath of the Covid-19 Pandemic – were inundated with elevated labor costs, negative operating margins, and adapting to their “new normal.” By the 2024 survey, although labor costs remained elevated, operations stabilized as volumes returned to "pre-pandemic" levels. Payor relations were at a critical point and interest rates were on the rise, yet, there was a sense of relief. The 2025 survey was the first where mid-sized providers’ top concerns deviated from those of larger health systems. While mid-sized health systems and single site hospitals were still focused on managing costs and payor reimbursements, the largest health systems were starting to look long-term to strategic priorities and technology investments, as evidenced by the record new money issuances in the healthcare municipal markets.[1]

After a volatile 2025, riddled with economic and legislative uncertainty from tariffs and the passing of H.R. 1, respondents in 2026 were, once again, broadly aligned on their top short- and long-term concerns, regardless of size. Notably, the highest short- and long-term concern for the majority of respondents was the impact of the current administration, especially as it relates to Medicaid enrollment, Medicaid reimbursements, and ACA subsidies. Labor, although materially improved since the inception of the Provider Survey, remains a top short- and long-term concern – a trend that is likely to continue into the foreseeable future. Payor relations and inflation are also top of mind for providers, with inflation of slightly more concern for mid-size hospitals and health systems. This article aims to outline the survey results, while providing insights into what the results mean for providers across the country, based on perspective provided by survey participants.

The 2026 PNC Healthcare Provider Survey engaged 30 hospitals and health systems across the country through in-depth ~60-minute discussions with system-level financial executives. This year, 70% of respondents have greater than $2 billion in annual revenue. As part of the survey, we had each of the participants rank their top short- and long-term concerns from the following list: Impact of current administration, Technology infrastructure, Labor, Relationships with payors, Inflationary pressures, Competition from alternative care providers, Industry Consolidation, and Interest Rates. Charts 1 and 2 show the share of respondents who ranked each category among their top three short‑ and long‑term concerns, segmented by provider revenue size. The results are as follows:

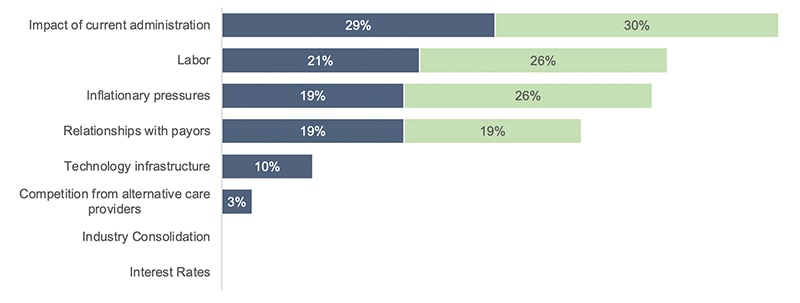

Top Three Short-term Concerns

(providers with > $2B revenue)

- 29% – Impact of current administration

- 21% – Labor

- 19% – (tie) Inflationary pressures & Relationships with payors

Top Three Short-term Concerns

(providers with < $2B revenue)

- 30% – Impact of current administration

- 26% – (tie) Labor & Inflationary pressures

- 19% – Relationships with payors

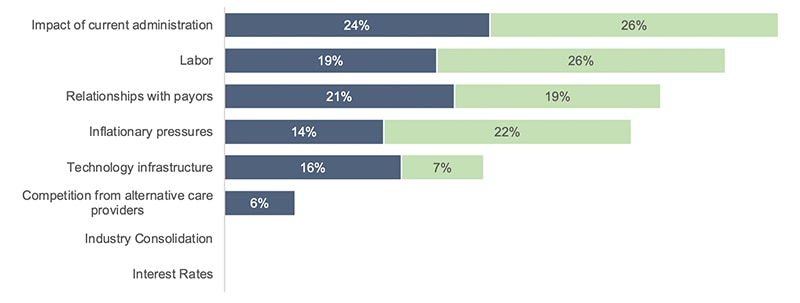

Top Three Long-term Concerns

(providers with > $2B revenue)

- 24% – Impact of current administration

- 21% – Relationships with payors

- 19% – Labor

- Worth mentioning: 16% – Technology infrastructure

Top Three Long-term Concerns

(providers with < $2B revenue)

- 26% – (tie) Impact of current administration & Labor

- 22% – Inflationary pressures

- 19% – Relationships with payors

Chart 1. Top Short-Term Concerns Ranked by System Revenue Size

Source: 2026 PNC Healthcare Provider Survey

View accessible version of this chart.

Chart 2. Top Long-Term Concerns Ranked by System Revenue Size

Source: 2026 PNC Healthcare Provider Survey

View accessible version of this chart.

Key Takeaways

Four key themes emerged from our discussions that shed some light on what is really driving healthcare providers’ concerns:

1. Impact of Current Administration Policies and Geopolitical Risks

In this year’s survey, the impact of the current administration emerged as the top short- and long-term concern across mid-size and large hospitals and health systems. Providers cited uncertainty stemming from changes to Medicaid eligibility and enrollment requirements, the sunsetting of enhanced ACA subsidies, and potential modifications to the 340B Drug Pricing Program as primary drivers of this concern (note that after the survey concluded, HHS announced it was cancelling its existing plans for a rebate model). Respondents emphasized resilience and scenario modeling while tactically avoiding predictions about policy outcomes; moreover, most respondents expect a rise in self-pay and uninsured patients presenting at higher acuity as a result of care deferral. To mitigate these pressures, organizations are implementing strategies that include: (1) strengthening eligibility support and financial advocacy to maintain patient enrollment, (2) pursuing cost containment and operational efficiency initiatives, and (3) conducting proactive modeling and multiyear planning exercises. Shifts in payor mix are expected to compress operating margins, straining health systems at a time when many of the individuals they serve are facing heightened Medicaid pressures and rising ACA premium costs.

2. Persistent Labor & Inflationary Pressures

Labor and inflation remain among providers’ top concerns in this year’s survey and are viewed as long‑term, structural issues for the healthcare industry. Although labor strains have eased from their COVID‑era peak, inflationary wage growth has kept labor as hospitals’ largest expense, and in some geographies, the high cost of living and housing affordability have further constrained labor supply. Inflation is also affecting non‑labor costs as providers report inflationary disruptions across supply chains, pharmaceuticals, and capital projects. To navigate these pressures, providers cite strategic actions such as structuring payor payments to automatically adjust with the system’s cost base and partnering with local nursing schools as talent pipelines, to more tactical measures such as targeted use of contract labor, and the deployment of productivity tools and automation to reduce manual administrative work.

3. Providers Continue to Navigate Volatility in Payor Relationships

In this year’s survey, both mid-size and large health systems identified relationships with payors as a continuing operational challenge. Some respondents reported a sharp rise in claim denials, reimbursement delays and underpayments prompting organizations to build and implement more sophisticated denial‑management programs including AI‑enabled tools to automate and accelerate appeals. Many noted mid‑contract policy changes and shifting reimbursement processes that complicate financial forecasting and strain operational stability. In response, systems are increasingly leveraging their scale, strengthening data preparation, and adopting more structured negotiation strategies to counter rising volatility. Overall, providers surveyed emphasized that payor relations are a critical work in progress amid a myriad of ongoing industry shifts.

4. Strategic Investments in Technology Become Healthcare’s Most Reliable Tailwind

Survey respondents identified technology infrastructure as one of the industry’s most promising yet complex near‑term opportunities, particularly AI adoption and cybersecurity preparedness. Many emphasized a “not‑if‑but‑when” mindset around cyberattacks, prompting renewed focus on business‑continuity exercises, redundancy planning, and investing in proper security controls. Still more respondents noted the creation of internal monitoring programs and data governance committees to work on the prevention of such attacks. In terms of AI adoption, about 30% of respondents highlighted ambient listening and documentation tools as some of the highest‑ROI AI applications, easing the documentation process in physician practices and gradually eliminating manual work. Providers are increasingly using AI tools to streamline processes and improve financial performance across denial management, revenue cycle operations, and customer service. Several respondents also noted plans to eventually apply these tools to internal data and within their finance teams. Hedging their positive outlook, some leaders caution that implementation discipline remains critical, noting that technology can quickly become cost‑prohibitive without a clearly defined business need. As a result, some systems favor AI capabilities embedded within existing platforms, such as EMRs, to minimize integration expenses. Overall, respondents described technology and AI as healthcare’s most promising near‑term tailwind, offering significant efficiencies and security when paired with strategic investment and strong infrastructure.

Providers continue to operate in an environment where legislative ambiguity, shifting dynamics in payor relationships, labor challenges and rising costs are compounding while organizations also strive to invest in advanced technology and cybersecurity to remain competitive and gain efficiencies. These challenges affect providers of all sizes, and the path forward demands adaptability and strategic focus. As providers navigate this complex landscape and prepare for continued volatility, PNC Healthcare remains committed to being an industry thought leader and strategic partner, supporting providers through the challenges ahead.

We would like to thank all the organizations who participated in the 2026 PNC Healthcare Provider Survey for their valuable insights. We sincerely appreciate your time and continued partnership.

Chart 1. Top Short-Term Concerns Ranked by System Revenue Size (view image)

| Short-Term Concerns (aggr) | Greater than $2B | Less than $2B |

| % of Aggr 1 | % of Aggr 2 | |

| Interest Rates | 0% | 0% |

| Industry Consolidation | 0% | 0% |

| Competition from alternative care providers | 3% | 0% |

| Technology infrastructure | 10% | 0% |

| Relationships with payors | 19% | 19% |

| Inflationary pressures | 19% | 26% |

| Labor | 21% | 26% |

| Impact of current administration | 29% | 30% |

Source: 2026 PNC Healthcare Provider Survey

Chart 2. Top Long-Term Concerns Ranked by System Revenue Size (view image)

| Long-Term Concerns (aggr) | Greater than $2B | Less than $2B |

| % of Aggr 1 | % of Aggr 2 | |

| Interest Rates | 0% | 0% |

| Industry Consolidation | 0% | 0% |

| Competition from alternative care providers | 6% | 0% |

| Technology infrastructure | 16% | 7% |

| Inflationary pressures | 14% | 22% |

| Relationships with payors | 21% | 19% |

| Labor | 19% | 26% |

| Impact of current administration | 24% | 26% |

Source: 2026 PNC Healthcare Provider Survey