Canada’s payments environment shares many similarities with the U.S., but key operational differences influence how companies send, receive, reconcile and protect funds. For U.S. organizations expanding north, the biggest adjustments may come from how Canadian payment rails are structured, how data is carried and how certain treasury services differ. Keeping these nuances in mind can help companies avoid friction and adapt processes smoothly as they begin operating in Canada.

For companies looking to expand into Canada, here’s an overview of Canada’s payment rails and solutions.

1. Dual Currency Support (CAD and USD)

Canada supports banking, payment clearing and settlement in both Canadian dollars (CAD) and U.S. dollars (USD) across wires, AFT (Canada’s version of ACH) and cheques. Canadian USD clearing systems are entirely separate from those in the U.S. (the Federal Reserve, The Clearing House), which means U.S. and Canadian USD transactions follow different processing rules.

2. Payment System Comparison

Payment Rails | Canada | United States |

Wires |

|

|

ACH / AFT |

|

|

Cheque Clearing |

|

|

Instant Payments |

|

|

Debit/Credit Networks |

|

|

* Banks in Canada typically post inbound AFTs same day or next business day. PNC offers same‑day posting to provide liquidity in the shortest window.

3. Payments Canada: The Core of the System

Payments Canada operates the country’s national clearing and settlement infrastructure —including AFT, Lynx and ACSS — and sets the rules that govern Canadian payments. Its role is comparable to Nacha in the U.S. ACH ecosystem, but the operating model and rules are not the same.

As a result, there are several structural and rule-based differences between Canadian and U.S. payment systems, including:

- Return windows

- Cutoff times

- PAD (Pre‑Authorized Debit) authorization and return rules

- Addenda limitations

- Settlement timing

Modernization of the Canadian payments ecosystem is underway, including work to launch RTR, Canada’s real-time payments system, which will introduce additional distinctions from U.S. instant payment rails once live.

For more information on Payment systems and rules in Canada refer to Payments Canada website: https://www.payments.ca/.

4. Payments Automation & Outsourcing (Integrated Payables)

U.S. and Canadian payments automation are increasingly aligned. Companies can send Integrated Payables transmissions to initiate ACH/AFT, wires, cheques/checks or card payments for both countries.

- Canada uses AFT and CPA 005; the U.S. uses ACH/Nacha

- Both markets support flat file, DSV and ISO 20022 XML formats

- APIs and ERP/TMS connectors are widely available in Canada

- Cheque outsourcing is available in both markets. Banks like PNC can print and mail CAD or USD cheques drawn on Canada accounts, and can print U.S. checks domestically within the U.S.

As ISO 20022 adoption grows across North America, companies can increasingly leverage one pipe, one platform and one process for automating payments.

5. Cheque Payments

Cheques remain a major payment channel in Canada, with 278.9 million cheques and similar paper-based payments used in 2024, according to Payments Canada¹. While electronic options continue to reduce overall cheque volumes, usage remains significant, especially for B2B payments.

- Canada processes cheques overnight with no float, influencing cash‑management timing

- Controlled disbursement does not exist in Canada (a feature unique to the U.S.)

6. Fraud Prevention

Fraud protection in Canada varies from the U.S. due to differences in the payments infrastructure. Canadian banks — including PNC — offer Cheque Positive Pay and ARP to mitigate cheque fraud. Canada also provides AFT Debit Blocks, although with fewer filter options compared to the U.S. While U.S. fraud tools cover both ACH and cheques, Canada’s fraud capabilities remain primarily cheque‑focused and governed by strict Payments Canada standards.

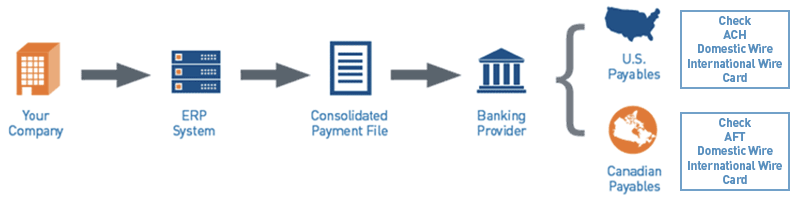

Figure 1: Integrated Payables Example Diagram

View accessible version of this chart.

7. Receivables (Lockbox, Remote Deposit, Electronic AR)

Lockbox services can accelerate cheque processing, improve cash flow, reduce costs and enhance security by centralizing and automating payment collection across borders. PNC’s Toronto lockbox site offers solutions for processing both CAD and USD cheques. Lockbox services in Canada allow U.S. companies to outsource receivables processing and provide a local mailing address for cheques vs. sending cross border.

Canada, like the U.S., offers remote deposit solutions. In Canada, the service is offered for CAD and USD cheques. Some banks can process USD checks drawn on a U.S. bank on their remote deposit solution. Cross-currency cheque processing (e.g., USD to CAD) may also be supported.

Electronic A/R like AFTs carry limited addenda, so supplemental information, such as email remittance or manual matching, is often required. This is a key operational difference from U.S. ACH.

8. Commercial Card Payments

Visa, Mastercard and AmEx are widely used in Canada. While U.S. and Canadian card programs run on separate card platforms, PNC can manage them together through a single digital interface, giving clients a unified view of spend management across both countries.

9. Information Reporting

Both countries support the same reporting file types — BAI, ISO 20022 (camt.052/053/054), EDI and APIs — but data content differs because the underlying rails differ.

- Both support current day and prior day reporting

- API‑based reporting is available in both markets

- ISO reporting may vary by bank due to slightly different structures with Payments Canada standards

10. Liquidity Management

Canada’s liquidity tools resemble those in the U.S., with differences in interest and account structure.

- CAD and USD operating accounts are common and allow cross‑border cash‑flow support without forced FX conversions.

- Canada may apply debit (negative) interest when accounts become overdrawn; this is available only to qualified customers.

- Earnings credit is available in Canada, but is less common than in the U.S.

- ZBA structures exist for both CAD and USD, enabling daily sweeping and centralized liquidity, though operational rules differ from U.S. ZBAs.

Let’s build your brilliant

Established in 1998, PNC Bank Canada is uniquely positioned to serve companies operating in both Canada and the U.S. Through a unified North American platform—and a single PINACLE® experience for payments, receivables, and reporting—PNC supports seamless cross‑border treasury operations.

U.S. companies exploring Canadian banking solutions can contact their PNC Relationship Team or visit pnc.com/canada.

Source

1. Automated Clearing Settlement System (ACSS) statistics, Payments Canada, January 17, 2025

Accessible Version of Chart

Figure 1: Integrated Payables Example Diagram

Automatic disbursement of payments via the consolidated payments file, made possible by your company’s ERP system connection to your banking provider. In the United States, your consolidated payment file would include check, ACH, Domestic Wire, International Wire and Card. In Canada, your consolidated payment file would include cheque, AFT, Domestic Wire, International Wire and Card.