Donor-advised funds (DAFs), as a unique type of charitable giving vehicle, require a specialized approach to strategic asset allocation decisions. At a basic level, DAFs need to be open to unlimited donors, each of which can have unique charitable intentions, time horizons, and risk tolerances. As a result, a sponsoring charity may need to provide a spectrum of asset allocation recommendations built for the diverse objectives and constraints of its donor base.

Below, we describe the basic features of DAFs, the key factors that may be considered in the asset allocation decision for a given donor, and how PNC Institutional Asset Management® structures portfolio recommendations for our clients.

Donor-Advised Funds: The Basics

A DAF is a separately identified fund that is maintained and operated exclusively by a section 501(c)(3) nonprofit organization, also known as the sponsoring organization. Once a donor makes a contribution, the sponsoring organization has legal control over that contribution, while the donor retains advisory privileges with respect to distribution of funds and the investment of assets in the account.[1]

One advantage of this type of charitable vehicle for donors is that the sponsoring organization is responsible for handling the investment along with the administrative and compliance responsibilities for that investment, and its associated costs. With that said, the drawback is that while the donor retains advisory privileges and the sponsoring organization will generally follow donor requests, the donor is giving up ultimate control of the assets. This is why we believe it is especially important that sponsoring charities demonstrate responsible stewardship of those assets.

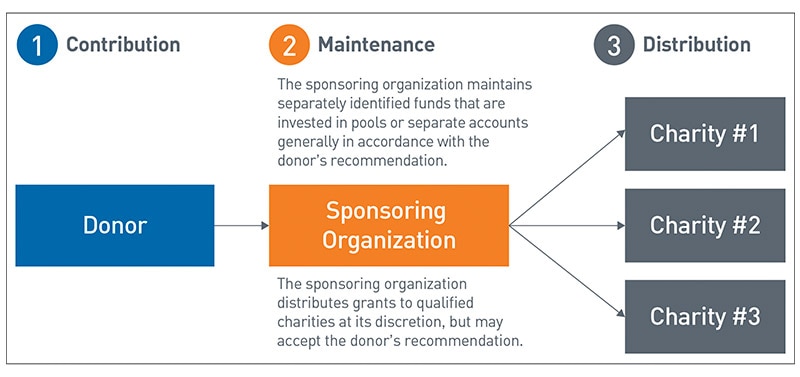

Figure 1: DAF Process

Source: PNC

View accessible version of this chart.

Managing Investment Policy:

Some Factors to Consider

When managing any individual investment program, there are certain factors that we believe are important when making decisions around proper portfolio positioning. For DAFs, this requires creating a spectrum of asset allocation recommendations built for a range of different objectives and constraints. The chart below illustrates how the range of asset allocation options might look.

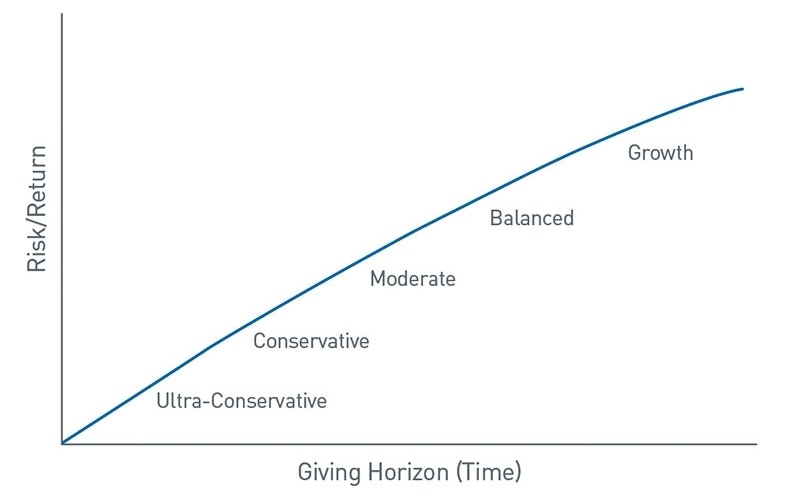

Chart 1: Possible Range of Asset Allocation Options

Source: PNC

View accessible version of this chart.

Outlined below are five key factors which may be important to address during the asset allocation discussion with a donor.

1. Donor’s Intentions/Time Horizon

The first question to ask for a given donor centers on determining the donor’s intentions. Specifically, is the donor planning to distribute all of the funds immediately or over the near term, or do they intend for the fund to last for several years, their lifetime, or over several generations?

The answer to this question, specifically regarding time horizon, is important. All things being equal, the longer the time horizon, the greater the ability to take on risk. This is because the longer time horizon allows the assets to “ride out” short-term market volatility, allowing for a higher equity allocation.

For donors who intend to distribute the entirety of their fund within a few years, it might be appropriate to be invested in a portfolio with a less risky asset allocation (i.e., one with a high level of shorter duration, investment-grade fixed income). Conversely, on the other end of the spectrum, are donors who want to grow their assets over 20 years without making any major distributions along the way. For these donors, it might be appropriate to be invested in a portfolio with a more aggressive asset allocation (i.e., with a heavy allocation to public equities). Donors who intend to make an annual distribution in perpetuity, such as 4% of the market value of their portfolio each year, might fall somewhere in the middle of the spectrum with a more balanced allocation intended to preserve purchasing power and allow for modest growth.

Framing these conversations with donors in the right way can be one of the most important inputs in the investment process. Further, it can help instill confidence that your organization cares about its donors’ intentions and is knowledgeable in how to help them achieve their objectives.

2. Return Objective

The return objective should be based on the donor’s intentions/time horizon mentioned above: If the intention is for the fund to maintain a distribution in perpetuity while preserving purchasing power, the chosen asset allocation will need to be able to achieve a minimum level of return.

Conversely, if a donor plans to distribute the fund over the next three years, such a time horizon might suggest the donor has lower return needs and might not need to pick a portfolio with aggressive growth objectives (and the higher volatility that often comes with a growth-oriented portfolio).

There is a wide range of return objectives possible — and, as we will discuss later, the different portfolio options typical to a given DAF allow for these different objectives. While there is no one-size-fits-all, a donor’s intentions and time horizon can help a donor to determine the right return objective for their specific situation.

3. Risk Tolerance

A donor’s risk tolerance is an important factor to gauge from both objective and subjective perspectives. On an objective level, the appropriate amount of risk relative to the donor’s return/distribution objectives can help increase the probability of the donor achieving those results. On a subjective level, a donor’s personal views on risk are important as well: If an account experiences outsized or unexpected levels of volatility, it could negatively impact the donor’s experience with the DAF as a charitable giving vehicle.

While determining risk tolerance might be best described as equal parts art and science, the inclusion of risk tolerance in the portfolio selection process can help to balance the objective and subjective considerations relevant to determining the right portfolio for a given donor. Specifically, risk tolerance helps with setting and managing expectations for the performance of the portfolio ahead of time, and can be instrumental in measuring and defining success over time.

4. Liquidity

Liquidity is an important consideration with the investment of DAFs, as distributions can be requested at any time. Given the potential for an erratic frequency of distributions, we think DAF pools should only be invested in liquid, readily marketable securities. Specifics around distribution needs may also factor into asset allocation decisions given the need to balance staying fully invested with the ability to liquidate investments for the cash necessary for distributions.

5. Unique Circumstances

The past decade has seen a remarkable growth in responsible investing assets. As a result, many DAFs have provided responsible investing portfolio options to their donors. An example of this type of portfolio option would be one that requires investments that screen for environmental, social, and governance criteria.

Responsible investing can be attractive to donors who are looking to align their investment portfolio with their personal values or intentions. It is important to understand what your donor base might be interested in and provide an appropriate investment portfolio option or options.

In summary, these five factors form a framework by which donors can be matched with a portfolio suited to their objectives and constraints. In the next section, we will discuss some sample donor scenarios and how they might map to different portfolio objectives.

Sample Donor Scenarios

As we have discussed, we feel it is important to have a range of portfolio options available to match the widest range of donor intentions and objectives. As you might expect, these portfolios should range from conservative to aggressive and provide a reasonable number of investment pools. Reasonable means neither so few that donors cannot choose one that fits their needs, nor so many that the management of the DAF as a whole becomes difficult or the pools end up too small to take advantage of economies of scale.

In the table below, we provide some examples as to how different donor time horizons and intentions might map to a given portfolio orientation. As a note, these are only examples and are meant to be directional rather than explicit recommendations. The ultimate decision is best made with a firm understanding of a given donor’s intentions and knowing the actual portfolio pools that are a part of your DAF.

Table 1: Donor Time Horizons and Intentions

| Time Horizon | Donor Intention | Return Objective/ Risk Tolerance | Portfolio Orientation |

1-3 years | A donor would like to give out money immediately to address a specific need, such as supporting a food bank during an economic downturn | Low/Low | Conservative |

| 1-10 Years | A donor would like to distribute the fund in annual installments to a charity over a set period, such as 7 years | Medium/Low | Balanced |

| Perpetuity | A donor and future generations would like to have money available to make periodic distributions to charity with no set frequency or distribution percentage. | Medium/Medium | Balanced |

| Donor’s Lifetime or Perpetuity | A donor would like to make a charitable distribution of 3.5% of the market value of their fund, while preserving purchasing power, in perpetuity. | Medium/High | Growth |

| 20+ Years | A donor would like to make a donation now and have it grow tax-free for 20 years before making a donation to a nonprofit organization of their choice. | High/High | Aggressive |

Source: PNC

Summary

The DAF as a charitable giving vehicle is understandably popular given its ability to satisfy a wide range of donor objectives and constraints. Having an investment policy framework that can accommodate a spectrum of donor intentions can help donors be successful in meeting their objectives and allow a sponsoring organization to have an effective and long-lasting charitable solution for its donors.

For more information, please reach out to your PNC Investment Advisor.

About Us

The Endowment & Foundation National Practice Group

The Endowment & Foundation National Practice Group builds on PNC Bank’s long-standing commitment to philanthropy and is focused on endowments, private and public foundations, and nonprofit organizations. Our group is structured to help these organizations address their distinct investment, distribution and capital preservation challenges. For more information, please contact Chris McGurn at christopher.mcgurn@pnc.com or Henri Cancio-Fitzgerald at henri.fitzgerald@pnc.com.

Accessible Version of Charts

Step 1: Donor makes a contribution to a sponsoring organization.

Step 2: The sponsoring organization maintains separately identified funds that are invested in pools or separate accounts generally in accordance with the donor’s recommendation.

Step 3: The sponsoring organization distributes grants to qualified charities at its discretion, but may accept the donor’s recommendation.

A longer time horizon for investing allows a donor to have a greater ability to take on risk and the ability to see more growth.

For example, a donor with a very short time to invest would likely fall into the Ultra-Conservative asset allocation.

The other asset allocations, in order of increasing risk and return, are: Conservative, Moderate, Balanced, and Growth.