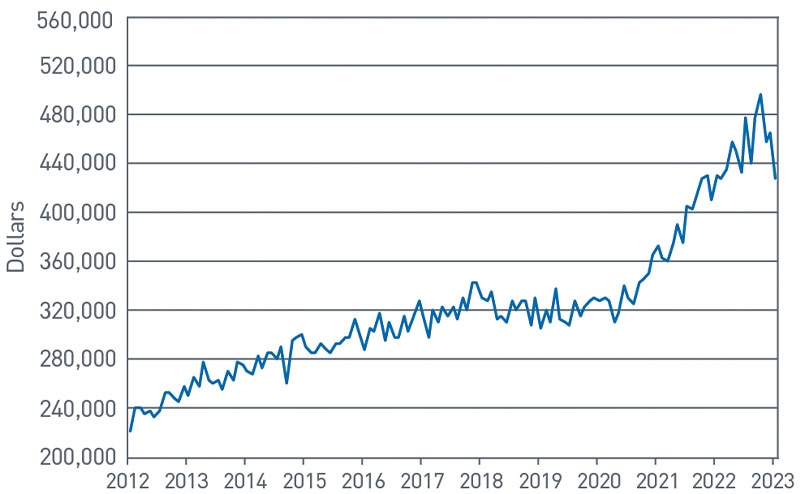

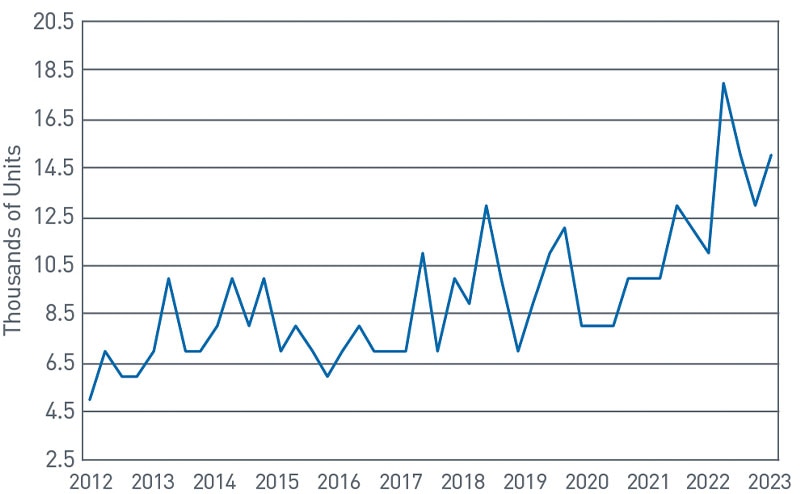

Prices for houses continued to rise through the end of January 2023, along with the percentage of houses purchased with cash. Charts 1 and 2 illustrate these two facts.1

We’ve all heard the stories. The previously hot real estate market had resulted in the inevitable bidding wars, giving cash buyers an advantage over those buyers that must qualify for a mortgage. To some extent, this is still the case, as the number of all-cash sales in January 2023 was up 4% year over year.2

Chart 1: Median Sales Price of Houses Sold for the United States

Source: U.S. Census, Department of Housing and Urban Development

View accessible version of this chart.

Chart 2: Houses Sold by Type of Financing, Cash Purchase

Source: U.S. Census, Department of Housing and Urban Development

View accessible version of this chart.

Raising Cash

If coming to the table with cash gives you an advantage over other potential buyers, PNC Private Bank® can help you raise it. One way to have cash ready when you make an offer to purchase a residence is to borrow secured by other assets, such as securities. If you own securities in a PNC Private Bank investment account, you can quickly borrow cash secured by the value of those securities3 through a Quick Link Portfolio (QLP) line of credit. A QLP line of credit gives you a fast way to access cash and can be put in place at any time without any origination costs. The line allows you to be ready for almost any contingency4 by being able to immediately access cash by drawing on the line. Unlike many credit solutions that can require extensive underwriting, a QLP line of credit requires minimal underwriting and can be established quickly. Approval requires only a review of your credit report and FICO score and validation of the market value of the eligible securities in your investment account. You show up as a buyer with “cash in hand.” The amount available to draw on your line of credit will vary based on the types of securities and their concentrations in your portfolio.5 Only after it is drawn will the line accrue charges, payable monthly and, in some cases, interest only. Importantly, even though your line of credit is secured by the assets in investment account, there is no disruption to those investments or to your long-term asset allocation and you can continue to trade in the account as long as minimum maintenance levels are maintained.

Is the Interest Deductible?

Your tax advisor can provide a complete review of the rules regarding the deductibility of debt used to purchase a home.6 Nevertheless, the following are a few things to remember about debt used to purchase a new residence. Only the interest on certain debt used to acquire a residence is deductible.7 Under current law, interest on debt used to purchase a residence after December 31, 2017, and before January 1, 2026 may be deducted8 if:

- The residence is a “qualified residence”, which means the taxpayer’s principal residence9 and one other residence selected by the taxpayer and used by the taxpayer as a residence.10

- The debt is “acquisition indebtedness,” which is any indebtedness “incurred in acquiring, constructing, or substantially improving any qualified residence of the taxpayer and is secured by such residence.”

- The acquisition indebtedness has a principal value of $750,000 or less ($375,000 or less in the case of a married individual filing a separate return).

- The “debt may be treated as incurred to acquire a residence to the extent of expenditures to acquire the residence made within 90 days before or after the debt is incurred.”11

As the line of credit is not secured by the residence, interest paid on that indebtedness may not be deducted as qualified residence interest.12 Nevertheless, because qualified acquisition indebtedness with respect to a residence can be obtained up to 90 days after acquiring the residence, it may be possible to obtain a home mortgage interest deduction when using the proceeds from a line of credit. In that case, the line of credit would serve as “bridge financing” allowing you to come to the table with cash, and later (within 90 days of closing) replace the outstanding line of credit with a loan secured by the residence (a mortgage) on which the interest paid qualifies for the home mortgage interest deduction.

The proceeds from your new mortgage would be used to pay-off the outstanding balance on the line of credit. When closing on a cash-out mortgage transaction within three months of an “all cash” purchase, PNC Private Bank clients are eligible for purchase loan-to-value limits and relationship pricing when assets are held at PNC Private Bank. The line of credit could remain in place, allowing you to draw upon it again for future cash needs.

Interest Cost

There are differences between the line of credit and a traditional mortgage. The interest rate charged on a line of credit is based on an establish market index interest rate plus a spread. The amount of the spread charged over the index rate can vary, for example a larger line of credit may carry a lower spread. Accordingly, the interest rate charged on a line of credit fluctuates as the index rate to which it is tied rises and falls. On the other hand, the interest rate charged on a conventional mortgage is typically fixed when the loan is made.

Cash When You Need It

The QLP line of credit provides you with a fast way to raise cash for any reason. In this highly competitive housing market, coming to the table with an all-cash offer can give you a competitive edge. Why not give yourself the flexibility to raise cash quickly by establishing a QLP? It could help you win the bidding contest for your next home. If you would like to learn more about the QLP line of credit or any other credit or cash management solution, contact your PNC Private Bank Banking Advisor or Relationship Strategist.

TEXT VERSION OF CHARTS

Chart 1: Median Sales Price of Houses Sold for the United States (view image)

| Year | Median Sales Price in Dollars |

|---|---|

| 2012 | 5,000 |

| 2013 | 7,000 |

| 2014 | 8,000 |

| 2015 | 7,000 |

| 2016 | 7,000 |

| 2017 | 7,000 |

| 2018 | 9,000 |

| 2019 | 9,000 |

| 2020 | 8,000 |

| 2021 | 10,000 |

| 2022 | 18,000 |

Chart 2: Houses Sold by Type of Financing, Cash Purchase (view image)

| Date | Median Sales Price of Houses Sold in United States |

|---|---|

| Jan 2012 | $221,700 |

| Aug 2012 | $253,200 |

| Mar 2013 | $257,500 |

| Oct 2013 | $264,300 |

| May 2014 | $285,600 |

| Dec 2014 | $301,500 |

| Jul 2015 | $292,300 |

| Feb 2016 | $305,800 |

| Sep 2016 | $314,800 |

| Apr 2017 | $311,100 |

| Nov 2017 | $343,400 |

| Jun 2018 | $327,500 |

| Jan 2019 | $305,400 |

| Aug 2019 | $327,000 |

| Mar 2020 | $328,200 |

| Oct 2020 | $346,900 |

| May 2021 | $390,400 |

| Dec 2021 | $410,000 |

| Jul 2022 | $478,200 |