When asked what aspects of an investment program are most important, most investment committees give answers that focus on the investment process, such as asset allocation, manager selection, and risk management. Answers that relate to investment philosophy, such as governance and oversight, tend to be given less frequently.

In this paper, we discuss the role of governance and oversight in helping institutional investment programs reach successful outcomes over the long term. Specifically, we focus on the importance of a robust investment policy statement (IPS), the relationship between goals/objectives and Enterprise Financial Modeling and the necessity of maintaining strategic continuity across generations of decision makers.

Maintaining a Robust Investment Policy Statement

Economic conditions, securities markets, people, and philosophies tend to be in a perpetual state of flux. Constant change can undermine an organization’s commitment to a long-term investment plan; however, when that organization has a comprehensive IPS that sets forth its long-term strategic direction, investment guidelines, and accountability standards, the course is well established and goals are more likely to be achieved.

So what makes an IPS robust? We like to answer the question with a simple litmus test: Could a stranger, whether a new board member or a new investment manager, pick up the IPS and reasonably understand how to manage the investment program? While the test may sound unlikely in principle, it is meant to illustrate how thorough the IPS should be. If it is important to the management of the investment program, it should be written down and described in this document.

For an IPS to be useful as an “instruction manual” for an investment program, there are some common sections we view as important when specifically focusing on nonprofit organizations: governance, objectives and constraints, portfolio parameters, risk management, client service, and acknowledgment. Taken as a whole, these sections start with the management of the portfolio, followed by its construction and the establishment of guidelines for monitoring and reporting. Finally, the acknowledgment serves to remind all involved parties of the agreement that has been put in place and their responsibility to act in accordance with that agreement. The IPS, and this acknowledgment, should be reviewed and acknowledged on at least an annual basis and ad hoc as warranted.

For more information on constructing a robust investment policy statement, please see our white paper, The Discipline to Succeed.

| I. Governance | II. Objectives & Constraints | III. Portfolio Parameters |

| a. Purpose & Scope | a. Statement of Goals | a. Asset Allocation |

| b. Investment Philosophy | b. Risk Tolerance | b. Benchmarks |

| | c. Liquidity Requirements | c. Selection and Retention |

| | d. Unique Circumstances | d. Types of Securities |

| IV. Risk Management | V. Client Service | VI. Acknowledgement of IPS |

| a. Control Procedures | a. Communications | |

| b. Performance Objectives | b. Reporting | |

The Relationship between Goals/Objectives and Enterprise Financial Modeling

Nonprofit organizations face numerous and specific challenges in pursuing their missions. These challenges, in addition to the ongoing risk associated with meeting the goals and objectives of an investment program, create an enterprise financial risk profile that should be incorporated into the strategic decision making process.

In a 2020 PNC survey of nonprofit institutions (n = 188), we asked two important questions:[1]

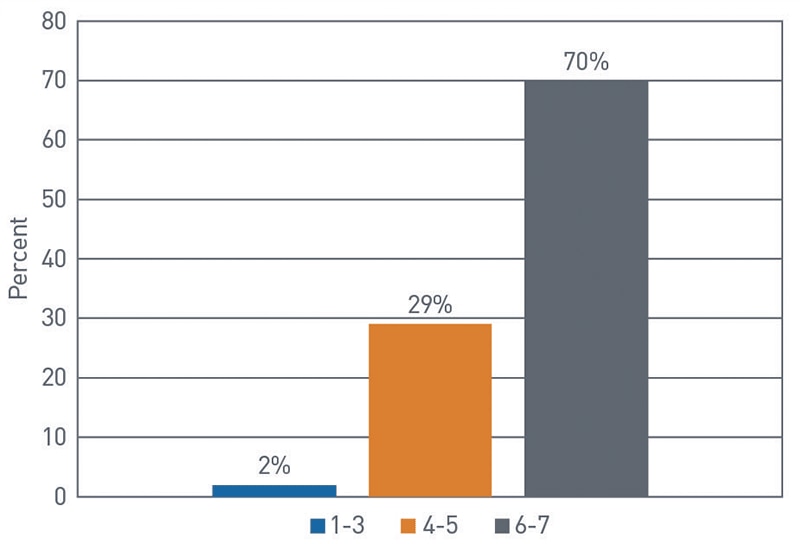

- Rate the level of value your organization places in advanced portfolio risk analysis (rank 1-7, with 7 being the highest). (Chart 1)

- To what extent does your organization adequately assess the role of investment risk? Rank 1-7, with 7 being the highest. (Chart 2)

Chart 1: Rate the Level of Value Your Organization Places on Advanced Portfolio Risk Analysis

Source: PNC; Numbers may not add up to 100% due to rounding

Chart 2: To What Extent Does Your Organization Adequately Assess The Role of Investment Risk?

Source: PNC; Numbers may not add up to 100% due to rounding

Based on the responses to the first question, the majority of respondents place a high degree of value on incorporating advanced portfolio risk analysis. However, in asking the second question, roughly a quarter of respondents aren’t confident that they are adequately assessing the role of investment risk in their portfolio.

In response to this desire for enhanced risk analysis and management, we are increasingly seeing institutional investors implement a goals-based analytical framework that helps to link enterprise financial strategy with the investment strategy. Specifically, this tends to be occurring in two ways:

- Analyzing the role of balance sheet investment assets in contributing to their financial wellbeing.

- Using the relationship between investment assets and financial results to help determine the best asset allocation for addressing liquidity and cash flow concerns.

Together, these two strategies form what we call Enterprise Financial Modeling. In this framework, the institution’s enterprise goals serve as a key component of the investment strategy for the asset pool(s).

Maintaining Strategic Continuity across Generations of Decision Makers

Organization’s long-term financial strategy is measured in decades — with that in mind, how do you incorporate the past and the future into today’s strategy? Many of us have experienced it: of the investment program, overall financial strategy, or even mission direction. This isn’t necessarily a bad thing — new team members are often important catalysts of change and improvement; however, sometimes this can inadvertently lead organizations to change or depart from longer-term strategies that aren’t properly documented or explained in a way that is evident in the review.

We propose the following example to illustrate this point: An investment committee targets a net annual investment return of 6% to support its spending policy, while accounting for inflation and fees, and is successful in achieving that target in a given year. Meanwhile, the broader equity markets post strong returns of 10% in that same year (we are choosing a short-term example for simplicity). From an outsider’s perspective or that of someone new to the board or investment committee, this might look like severe underperformance. In reality, the investment committee achieved its stated goal, likely with less risk than a portfolio targeting the 10% return of the broader equity markets would have taken.

To tackle the issue of strategic continuity across board and investment committee turnover or additions, there are two best practices that can help set your organization up for success: clear and complete documentation and board succession planning.

Clear and Complete Documentation

We discussed earlier the details that we believe are important for nonprofit organizations to include in their investment policy statements. In that vein, we strongly recommend that nonprofit organizations document their goals and objectives clearly in their IPS and set time to bring new board members up to speed on the entirety of the document. This documentation can help new decision makers to quickly come up to speed.

Board Succession Planning

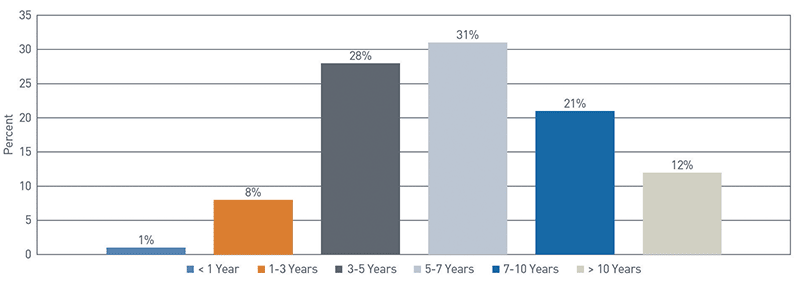

In our 2020 survey of nonprofit organizations (n = 188)

[1], we asked the question, “How long have you served as a leader with investment input at the nonprofit where you are involved in decision making about the endowment or foundation?”

Chart 3: How Long Have You Served As a Leader with Investment Input?

Source: PNC; Numbers may not add up to 100% due to rounding

The majority of respondents to this survey question indicated they have been with their nonprofit between 3 and 10 years, with 12% answering they’d been there longer than 10 years. The reason we bring up tenure is with regard to decision maker turnover: Whether a given nonprofit organization has term limits for board or investment committee members, the committee members leave/move naturally due to other responsibilities or employment changes, or even if board members are approaching retirement age and no longer want to take on management responsibilities, longer tenure can increase the proximity to turnover. With many respondents answering that they’ve been with their current nonprofit organization for a number of years, this might indicate that a new wave of changes to nonprofit leadership could be imminent. With that in mind, we suggest that nonprofit organizations have clear succession plans in place, including specifically the recruitment and education strategies intended for bringing onboard the next generation of decision makers.

Conclusion

A phrase that we’ve found to resonate with our clients is “being a nonprofit is a choice; generating revenue is not.” Bearing that in mind, it is important that nonprofit organizations focus on how they manage their financial resources to allow those resources to support their missions. With a focus on proper governance and oversight, nonprofit organizations can increase the likelihood that financial assets are successful in supporting and driving mission success.

Accessible Version of Charts

| < 1 Year | 1 - 3 Years | 3 - 5 Years | 5 - 7 Years | 7-10 Years | > 10 Years |

| 1% | 8% | 28% | 31% | 21% | 12% |