PNC and PNC HomeHQ are registered service marks of The PNC Financial Services Group, Inc. ("PNC"). PNC is a registered service mark of The PNC Financial Services Group, Inc. (“PNC”). All loans are provided by PNC Bank, National Association, a subsidiary of PNC, and are subject to credit approval and property appraisal.

PNC Escrow Guide

Understand your PNC escrow account and escrow analysis statement

Escrow

When your loan is created, PNC sets up an escrow account to allocate the funds to cover certain property-related expenses like taxes and insurance costs. As you make your mortgage payments, a portion is used to fund your escrow account. Then when the taxes and insurance bills are due, PNC uses the funds in your escrow account to pay for these bills.

This mortgage escrow account remains open for the loan term or until PNC and you agree to close the escrow account and have you pay the expenses directly.

Video: How Escrow Works

Homeowners

House is purchased with a mortgage through PNC.

Escrow Account

PNC opens up an escrow account.

Escrow pays:

- Homeowners Insurance

- Property Taxes

- Private Mortgage Insurance

Escrow Analysis Statement

The amount required in the escrow account could change if your property taxes and insurance go up or down – this may mean you have a shortage (not enough) or a surplus (too much) in your escrow account.

PNC reviews your account each year to make sure you’ll have enough to cover required costs and sends you an escrow analysis statement with the results of our review.

How We Balance Escrow Accounts

PNC estimates the new escrow portion of your mortgage payments, based on the annual tax and insurance payments from the previous year, then divided by 12 or by the number of the scheduled mortgage payments in a year.

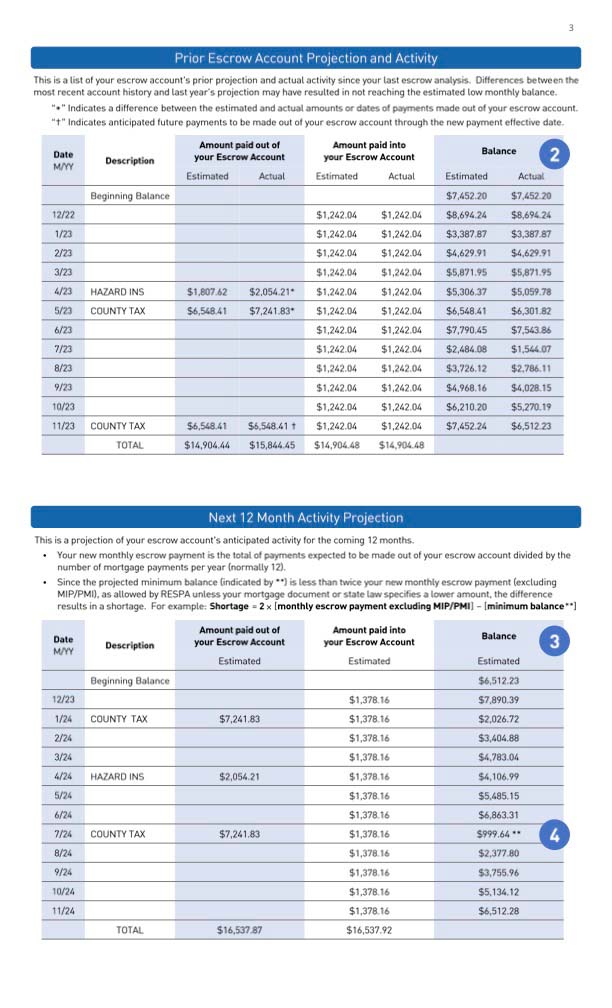

PNC prepares a prior year activity table to visualize any differences between previous year’s estimates and actual escrow transactions, all differences will present an asterisk (*) next to the amount. This chart also displays the final escrow account balance that will be used as a starting point for the next 12-month escrow projection.

PNC uses the estimated escrow payment from step 1 to forecast what will be paid into and out of the escrow account along with the estimated balance after each transaction for the next 12-months.

PNC marks with two asterisks (**) the projected minimum balance within the next 12-month projection.

PNC analyzes the projected minimum balance (indicated by **) and determines if:

- There is a shortage: the projected minimum balance is less than twice the new monthly escrow payment excluding MIP/PMI, unless your mortgage document or state law specifies a lower amount, the shortage will be spread over the next 12 months.

- There is a surplus: the lowest balance is more than twice the new monthly escrow payment excluding MIP/PMI. Unless your mortgage document or state law specifies a different amount, surpluses below $50 will be applied to reduce your payment. A check will be included in your statement analysis if the surplus is at/above $50. If your account is delinquent or not paid up-to date, connect with PNC once the outstanding payments are made, to have the surplus refunded or applied to future mortgage payments.

- The account is even: the lowest balance equals to twice the new monthly escrow payment, excluding MIP/PMI. Unless your mortgage document or state law specifies a different amount, neither a shortage nor a surplus exists.

FAQ

Have Questions?

We Are Here to Help

![]() ©2026 The PNC Financial Services Group, Inc. All rights reserved.

©2026 The PNC Financial Services Group, Inc. All rights reserved.

PNC Bank, National Association. Member FDIC

Read a summary of privacy rights for California residents which outlines the types of information we collect, and how and why we use that information.